- Low-cost carriers, such as Ryanair and EasyJet, rapidly gained market share within the commercial aviation industry

- Their strategy is all about cost cutting, expansion and targeting: no hubbing, no extras, no comfort with a predominant position in international flights

- Seems that tourism grows as ticket prices decrease: free fairs in the future?

The air industry in the EU employs between 1.41 million and 22 million people and overall supports between 4.83 million and 5.54 million jobs. The direct contribution of aviation to EU GDP is €110 billion, while the overall impact, including tourism, is as large as €510 billion through the multiplier effect. In fact, the availability of direct intercontinental flights is effectively a major determinant in the location choice of large firms’ headquarters in Europe: a 10% increase in the supply of intercontinental flights results in a 4% increase in the number of headquarters of large firms. A 10% increase in departing passengers in a metropolitan region increases local employment in the services sector by 1%.

During the last decades of the XX century, the market for the air industry was pretty much divided between the major state-owned companies like British Airways, Air France and the US-based ones, like Pan Am or Delta. The shift through privatization of airline companies and to the hub-and-spoke systems in Europe, where traffic is concentrated into a single, centrally located reduced the number of direct routes, and condensed traffic flows, permitting the use of larger aircraft and the operation at higher load factors. The hub is used as a connecting point for passengers travelling between any other pair of destinations in the network.

The full access to the EU aviation market (following the many phases of liberalization and deregulation of the market in the 90s) allowed low-cost carriers to fully penetrate the European market, including the Member States’ domestic markets. They took advantage of the opportunity to establish an ever-increasing number of crew and aircraft bases all over Europe, whereas the flag carriers remained designated to their national home bases. This was for operational reasons of hubbing as well as aero political reasons of nationally restricted traffic rights regarding intercontinental routes. Ryanair began its activity in 1985 with only 25 employees and a single aircraft and nowadays it is the largest European low-cost operator, accounting for 741 destinations and a team of more than 5000 employees. Its success is due to the pioneering role it played in the birth of another industry, the budget, or low-cost, industry.

Ryanair’s business model (and it applies to almost every low-cot company) is based on:

- Expansion: 1800 daily flights from 86 different bases (now probably more), connecting over 200 destinations in 33 countries. No central hub, unlike flag carriers, with huge negotiation power towards airports. In fact, Ryanair operates mainly from the smaller airports located near the big cities and many times is the only company, like Bergamo Orio Airport, considered to be Milan even though being in two separate cities 55km apart.

- Cutting cost: Ryanair operates with a fleet of over 400 Boeing 737 constantly renewed, eliminates some services and comforts traditionally offered free of charge (like meals and reclinable seats), sub-contracts some costly operations, limits the airport charges and, staff spending, has aggressive and efficient flight policies as well as the low costs of advertising.

- Internet: by 2007 (when, just as a benchmark, the first iPhone ever was sold), the airline was reporting over 90% of its direct sales to happen via the Internet. This method successfully implemented by Ryanair offered advantages both to the company and to the clients. Moreover, selling direct to the market enabled the company to have detailed market information concerning their customers.

- Target: the efficiency model inspired by Southwest airlines aims to pursue a cost-based strategy, offering the cheapest fares possible. The typical passenger is an individual that mostly travels for private purposes within Europe, for example, who visits friends and relatives or goes on city-sightseeing trips. That’s because they are price-sensitive with a lower income level or other preferences and less willing to pay for the add-on services onboard. The offer is compatible with this target, to not say it was built for it, as the remarkable flexibility granted by the multiple branches and identical planes combined with a focus on short international and national flights mainly in Europe increased cost-efficiency. The standardization of the process and the research for the economies of scale remind me a bit of the Ford production line.

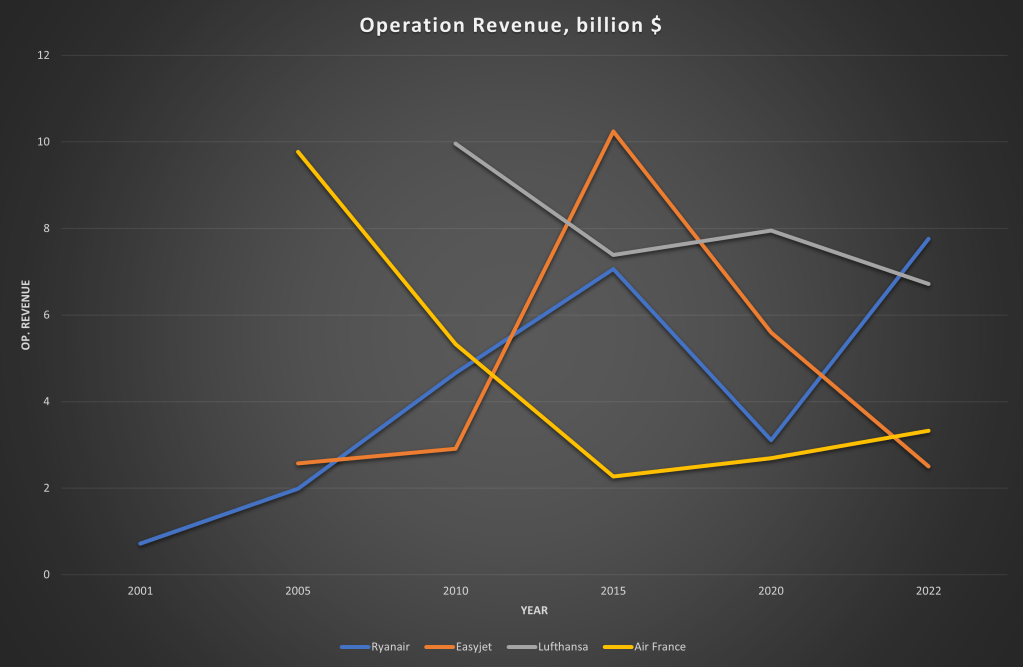

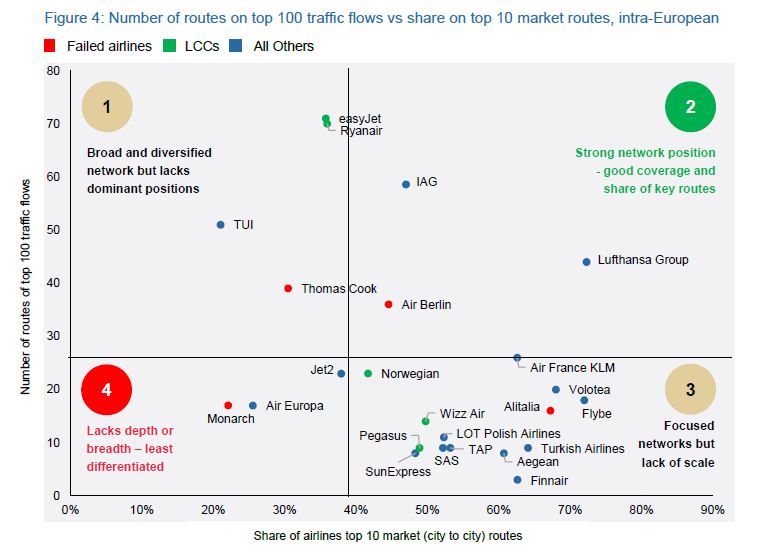

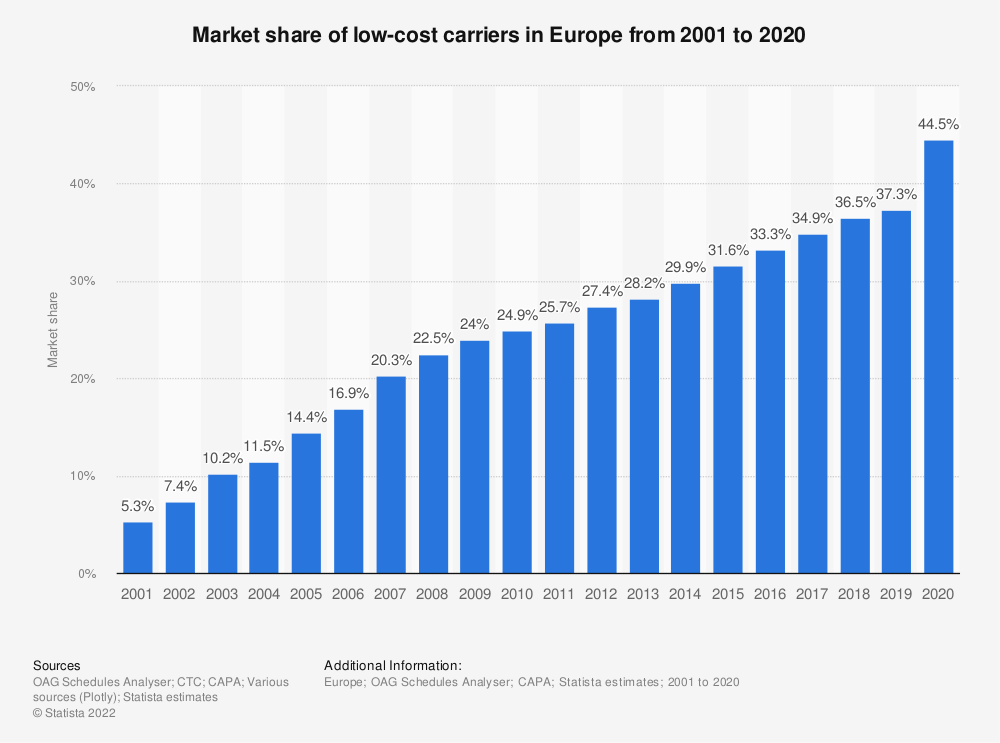

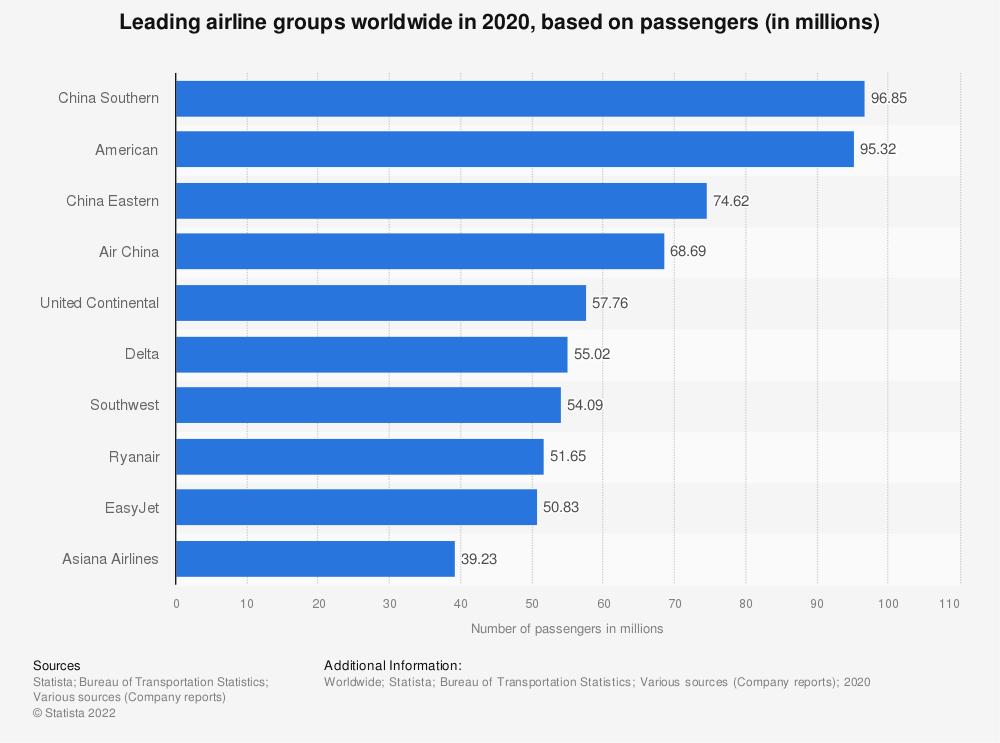

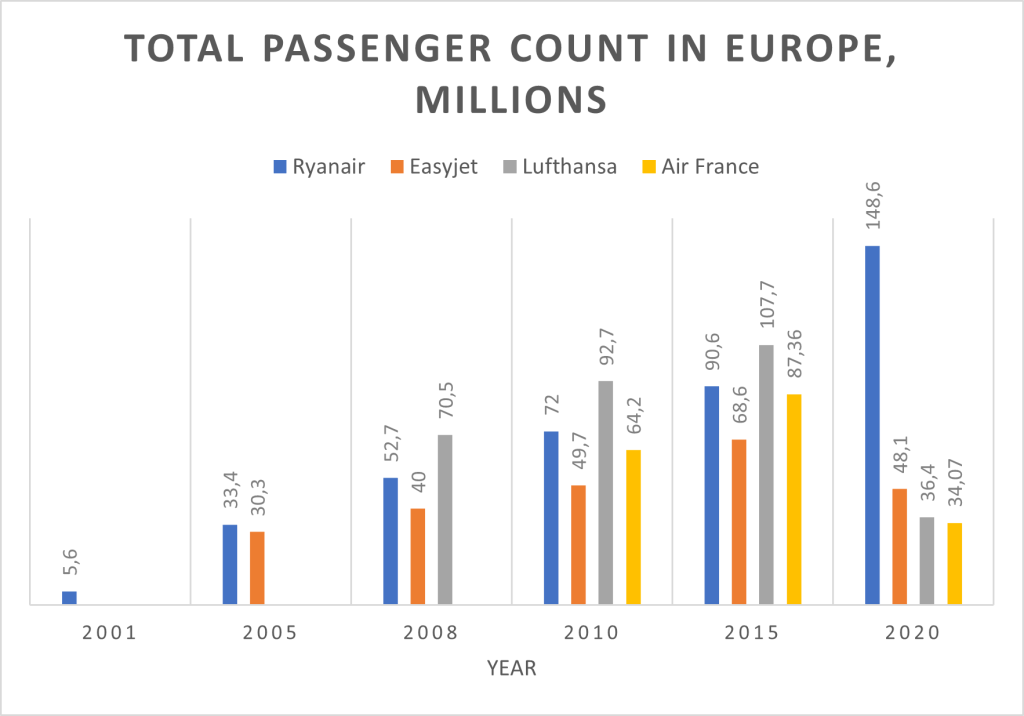

It appears clear that Ryanair, as well as EasyJet, Wizz Air and Vueling among the others, divided the air industry into two different industries, with different products, targets, and ticket prices. As for operational revenue, Ryanair is following a clear trend of growth that also extends to the total passenger count per year. The year-to-year fluctuations seem quite moderate, considering the sector. On the other side we find out that EasyJet and Lufthansa’s revenues varied a lot, and Air France follows a decreasing pattern. The data though is very comparable and similar regarding extraordinary occasions, for example in 2020. Passenger count is obviously related to the revenue and shares similar stats. The rest of the market is increasingly occupied by low-cost carriers, with an astonishing growth from 5.2% in 2001 to 44.5% in 2020. Looking at the market positioning we can notice how Ryanair and EasyJet are the ones with the most routes of all, while other companies like Turkish Airlines, Finnair and Air France tend to be more focused and less scalable. Furthermore, in 2021 Ryanair and Lufthansa were the first two companies in Europe as of passenger traffic (72.4m and 46.9m passengers).

What is the point then? The most important aspect to consider is that low-cost carriers changed the way and the frequency that people travel. Many would argue that the biggest airlines, first Ryanair, was lucky to find the right timing to enter the market: they may be unhappy with their non-reclinable and tiny seat, or because they have to take a plane departing at 5 am. The reality of things is that it’s not that easy to replicate their success. Cost-efficiency is achieved through a series of massive investments in aircrafts, harsh negotiations with airports and service owners and skilled and organized management. Competing for the best price is like this, whether you like it or not. It is as successful that even the most historic flag carriers started their line of low cost: Lufthansa launched Eurowings in 1993 and Germanwings in 2002, while AirFrance launched Transavia France in 2006- but let’s just say they are not going through a very profitable moment.

In the future, it is likely that the growth of low-cost market share (on international flights) will continue to increase, leaving the flag carriers more and more focused on the long intercontinental routes and niche business flights. Since no competition on cost can be achieved without cost-cutting on services, the average tourist will probably keep flying low cost and potentially begin to choose where to go after seeing how much the ticket is. This phenomenon, personally called “Fly first, then we’ll see”, is more and more popular among young individuals that don’t care about the comfort of a 2-hour flight: the demand is so high that companies literally create the routes because if people will go there cheaply, the local tourism will beneficiate from that. It’s not charity though: as Ryanair chief Michael O’Leary said at the Airport Operators Association conference in London (2016) “The challenge for us in the future is to keep driving air fares down. I have this vision that in the next five to 10 years that the air fares on Ryanair will be free, in which case the flights will be full, and we will be making our money out of sharing the airport revenues; of all the people who will be running through airports, and getting a share of the shopping and the retail revenues at airports.” Would you imagine travelling for free and not having to hide from the inspector?

RESOURCES:

https://www.teneo.com/european-aviation-perspective/

https://www.theguardian.com/business/2016/nov/22/ryanair-flights-free-michael-oleary-airports

https://companiesmarketcap.com/air-france-klm/marketcap/

https://www.irishtimes.com/news/ryanair-reveals-strong-2005-passenger-figures-1.767083

Traffic

“The Evolution of the European Low-cost Airlines’ Business Models. Ryanair Case Study” by Laura Diaconu, Alexandru Ioan Cuza University of Iasi, Romania, 2012

“EU Air Transport Liberalisation Process, Impacts and Future Considerations” by Guillaume Burghouwt, Pablo Mendes De Leon and Jaap De Wit, International Transport Forum, 2015

“The European airline industry: from single market to world-wide challenges”, Commission of the European Communities, 1999

“Strategic analysis of Ryanair” by George-Cristian Prichinet, Copenhagen Business School, 2020

“An Aviation Strategy for Europe”, European Commission, 2015

“Ryanair Group: Annual Report 2022”, 2022

Leave a comment