- To evaluate nuclear energy, its costs must be divided in uranium and nuclear plants construction. Both have some potential geopolitical risks.

- But costs aren’t all: sustainable energy as an alternative and the need for a fast change in energy mix bring up the number of nuclear energy projects, as China is doing.

- The organization of the state and the economy push have a strong influence on overall energy costs, resulting in developing countries adopting nuclear and developed ones not.

After analyzing the key aspects of the Italian energy market as well as the French’s, here we are. At the end of the first part of this research on nuclear energy, I suggested that more research has to be done regarding the real sustainability cause, the effects on energy prices to consumers and the effects on the energy market. Hence, here we are, welcome to the second part.

The major parts of the cost of nuclear energy are divided into nuclear plants and uranium. To produce energy uranium atoms (U3O8) are needed, as they are chosen for their ability to develop a nuclear chain reaction: in nuclear fission, atoms are split apart, which releases energy. All nuclear power plants use nuclear fission, and most nuclear power plants use uranium atoms. During nuclear fission, a neutron collides with a uranium atom and splits it, releasing a large amount of energy in the form of heat and radiation. More neutrons are also released when a uranium atom splits. These neutrons continue to collide with other uranium atoms, and the process repeats itself over and over again. Of course, this reaction is controlled in nuclear power plant reactors to produce a desired amount of heat. In addition, the uranium extracted from mines must undergo a process called “enrichment” and therefore enrichment plants are needed. According to IEA, in 2019 nuclear energy counted for 10.3% of total world energy production, mainly in North America and in the West & Central Europe areas, where more than half of the 429 operable reactors were located.

The world’s uranium mining is concentrated in Kazakhstan, Namibia, Canada, and Australia, while the overall uranium resources are, again, vastly in Australia (28%), Kazakhstan (15%) and Canada (9%), according to the WNA in 2019. In Europe, Ukraine is the only country with a noticeable disposal of uranium (2%) and mines for around 1000 tons of production (still around 1-2%). As Europe’s top producer of uranium, its supply was influenced by the Russian invasion the last spring and had an impact also on the uranium market. Globally, mobile uranium inventories have continued to decline at an accelerated rate over the last two years, driven by many factors, including COVID-19 pandemic production declines, the advent of the Sprott Physical Uranium Trust (SPUT), and strategic acquisitions by junior uranium companies to support future project financing efforts. SPUT purchased more than 24 million pounds U3O8 in 2021 or about 25% of all spot purchases. Through August 2022, the Trust has purchased an additional 16 million pounds U3O8 in the market. In addition, geopolitical risk has weighed heavily on the uranium market over the last several months, beginning with civil unrest in Kazakhstan in January 2022, followed by Russia’s invasion of Ukraine a month later. The spot uranium price, measured in USD/Lbs and averaging 28.87$ in the period 2018-2021, reacted strongly to Russia’s military action, increasing from $43.00 in late February 2022 to a peak of $63.75 in April. The spot price has since resided in the mid-to-high-$40s range. As a result of heightened geopolitical risk, many utilities are shifting their contracting focus to the term market to meet unfilled needs in the second half of this decade, and utilities with existing Russian enriched uranium contracts are actively seeking replacement supplies in the market. In recent history, the market for uranium, which, by the way, is not traded on an open market like other commodities but by private contracts, has peaked at least two times: September 2007 (commodities bubble) and January 2011 (Fukushima nuclear disaster). At any time, uranium supply remained stable as most power plants have long-term uranium delivery contracts (futures, hence why the price is “spot”). Trading Economics and Cameco forecast a growing trend in spot prices of uranium, estimating a range of 55-80$ until 2025. But, again, as a production factor, the uprising cost is not above the actual inflation rate and is comparable to market-exchanged commodities like natural gas and oil. The only other element left is the cost of the enrichment process and the intermediate process called conversion (basically, the removal of the impurities of mined uranium prior to enrichment), both of them up 136% (spot price, conversion) and 67% (spot price, enrichment) as of Q3 2022, while the global nuclear industry relies on Russia for approximately 14% of its supply of uranium concentrates, 27% of conversion supply and 39% of enrichment capacity. Among the majors entering the sector, it’s impossible not to mention China.

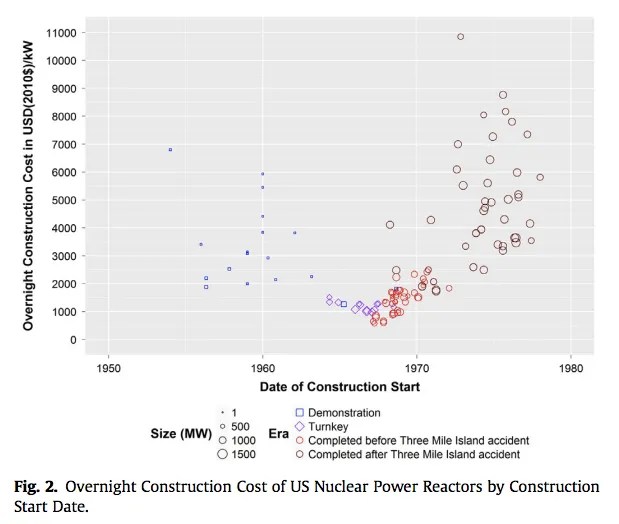

In reality, the biggest cost is the construction of nuclear plants. The convenience of this cost over other forms of energy plants is a complex matter, and the results depend crucially on location. For example, coal is, and will probably remain, economically attractive in countries such as China and Australia, as long as carbon emissions are cost-free or not fully cost. Generally, nuclear power plants are expensive to build but relatively cheap to run, even including waste disposal and decommissioning into the operating costs. If the social, health and environmental costs of fossil fuels are also considered, the competitiveness of nuclear power is improved. The main metric used to determine the convenience of an energy source is the Levelized cost of electricity (LCOE)* which matters the capital cost, usually in overnight costs (physical plant equipment, staff, supervision and so on) and eventual financing costs. Again, the location is crucial: as nuclear energy remains a capital-intensive technology, the discount rate of capital cost determines the economic viability of nuclear power across the world. The discount rate for nuclear construction projects in the United States is 12.5%, higher than in many other countries, especially those where the nuclear industry is at least partially subsidized by the government. For example, discount rates for plant construction are typically closer to 8% in France and just 2–3% in Japan. Furthermore, a NEA study on 22 countries in 2015 found that, at a discount rate of 10 per cent, the median cost of both natural gas and coal was lower than nuclear energy, while at a discount rate of 3 per cent, nuclear energy was the most economical option in all countries analyzed. Still, at more than that rate nuclear energy is still the second most convenient (up to 15% disc. rate) being second just to CCGT 2 (natural gas).

The average cost of building a nuclear power plant, which in the 1950s was seen as the miracle solution to global energy developments, is today much higher than expected. Of course, the latter depends on the type of plant and the deadlines to be respected, but in any case, the initial investment is very heavy. Thus, the investment costs for constructing the 58 reactors currently operating in France amount to nearly €96 billion. On the other side of the world, China has emerged as the world’s last great believer (after decades of cost overruns, public protests, and disasters elsewhere), with plans to generate an eye-popping amount of nuclear energy, quickly and at a relatively low cost. China’s ultimate plan is to replace nearly all of its 2,990 coal-fired generators with clean energy by 2060. To make that a reality, wind and solar will become dominant in the nation’s energy mix. Nuclear power, which is more expensive but also more reliable, will be a close third, according to an assessment last year from researchers at Tsinghua University. Financing at a bare 1.2% interest rate, China is planning to at least 150 new reactors in the next 15 years, more than the rest of the world has built in the past 35. The effort could cost as much as $440 billion; as early as the middle of this decade, the country will surpass the U.S. as the world’s largest generator of nuclear power. As of now, 46 reactors are planned or under construction.

But not everybody follows China’s example. For example, by the end of 2022, Germany is phasing out nuclear power. Since the first reactor started operations in 1955, the country had built more than 100 nuclear facilities, including power and research stations, and waste deposits. Direct and indirect German government subsidies alone, including research grants and tax credits, since the mid-1950s have added up to €287bn, FÖS has calculated. Another €9bn was spent on other costs for the state, such as police operations during anti-nuclear protests. The same situation is happening for generally Western countries and developed countries, like US and UK. According to forecasts from S&P Global Commodity Insights, as renewables capacity expands, the low marginal production costs will likely undermine long-term power prices in Western Europe. This means that direct state involvement, or at least financial and policy support, will be a key determinant for nuclear projects, alongside whether or not investors and operators have the appetite to take on the construction risks linked to nuclear new builds. And this is not even considering safety issues and consequent regulations that, especially in the US, skyrocketed the price of nuclear plants starting from the Three Mile Island accident (1979). Also, recent blackouts due to extreme weather have demonstrated the importance of firm power and a diverse energy mix.

Now comes the real costs. The cost to consumers is determined by factors like fuel, power plant costs, distribution system, weather conditions and regulations. Regarding the prices for households, the world average is 0.141$/kWh. As of March 2022, of the mentioned countries, France costs 0.185$/kWh; Italy costs 0.309$/kWh; Germany at 0.442$/kWh; UK at 0.279$/kWh; USA at 0.162$/kWh; China at 0.075$/kWh; Japan 0.221$/kWh. Adjusting those values to the inflation rate to have a broader overview of the prices, we further confirm our thesis: the trend is clear, as developing countries have way cheaper energy than developed ones, while they are the most carbon-emitting ones.

Overall, nuclear energy has a lot of requirements for a successful implementation:

- Low-interest rates (or statal subsides)

- fully operational capacity

- access to uranium sources, conversion, and enrichment plants

- retro dated energy mix (ex. China and coal), implying the highest emissions and fastest need to change the energy mix

While we stated that nuclear energy may be slightly cheaper and certainly less subject to geopolitical factors than oil or gas, the costs of starting nuclear plants from scratch are, as of now, utopic for a country like Italy. It is, instead, a great opportunity for developing countries to reduce their carbon emissions while supplying an increasing economy, that can grant full operational power to nuclear plants and the construction of complementary plants, for example for waste management and uranium enrichment. Among European countries, the solution to sustainability is to further implement renewable energy production, which generally can reduce geopolitical risks and potentially decrease energy costs due to less need for distribution and transmission facilities.

1 It is the total cost to build and operate a power plant over its lifetime divided by the total electricity output dispatched from the plant over that period, hence typically cost per megawatt hour. It takes into account the financing costs of the capital component (not just the ‘overnight’ cost).

2 combined cycle power plant

Epilogue:

This article was one of the most difficult projects that I ever made. Even though I tend to like taking on challenging tasks, I feel that more and more research can be done on this topic. Part 1 and Part 2 surely offered me the opportunity to analyze almost all the aspects to consider in order to implement nuclear energy but, since the number of variables, the results can change drastically. In the notes, you can find all the data supporting my thesis alongside the data underlying the “Energy prices to emissions” graph. Thank you very much for your attention. Goodbye.

SOURCES

https://www.eia.gov/energyexplained/nuclear/

https://www.uxc.com/p/products/rpt_umo.aspx

https://www.cameco.com/invest/markets/supply-demand

https://www.ompe.org/en/the-cost-of-nuclear-power-plants/

https://www.vox.com/2016/2/29/11132930/nuclear-power-costs-us-france-korea

https://world-nuclear.org/information-library/economic-aspects/economics-of-nuclear-power.aspx

https://www.oecd-nea.org/lcoe/

https://thebulletin.org/2019/06/why-nuclear-power-plants-cost-so-much-and-what-can-be-done-about-it/

https://www.globalpetrolprices.com/electricity_prices/#hl126

https://tradingeconomics.com/country-list/inflation-rate

data: Nuclear data.xlsx

Leave a comment