Worldwide, the Fintech market is a fast-growing industry, valued at USD 294.74 billion in 2023, and expecting to reach a valuation of USD 340.1 billion in 2024. Yes, billions. At the same time, Fintech companies are the ones delivering technology to every day’s life, from how people pay to how people invest their money. But what is exactly FinTech?

Let’s look into some literature: the term “Fintech” stands for “financial technology” and indicates all the applications of specialized computer software and algorithmic programmes to assist consumers, business owners and other individuals in better managing financial activities and processes (Mhlanga, 2023). More specifically, FinTech is part of the financial industry, and comprehends all the tools, platforms and ecosystems characterised by particularly innovative processes, applications, business models or products (Kaur et al, 2021). However, as the attribute of “innovative” could be misleading, it is common to associate the FinTech industry with the shift from Analogue to Digital finance and the mass adoption of devices like computers and mobile phones.

According to existing literature, there is not a unique point of view regarding its definition. By focusing on aspects like improving the efficiency of financial services with technology, hence contributing to the social welfare, Scheuffel (2016) defines FinTech as “a new financial industry that applies technology to improve financial activities.” On the other hand, Schindler (2017) questioned the feature of “new” by linking the evolution of this industry to the depth of innovation: in this sense, not only FinTech would be improving the financial industry, nor just implementing technology, but also altering its fundamentals and attributes. Furthermore, Arner et al. (2015) confuted the feature of “new” by tracing the journey of FinTech over the last 150 years, dividing its evolution into three phases, that finally combine in how we modernly think of the industry as digital financial services.

As it stands, FinTech is centred on three pillars: communication, technology, and finance. Communication applies to the relationship between the public and the financial services, which changed substantially with the technology innovations over the last centuries. On the other hand, financial services evolved as well, being mainly a customer-focused industry. In a nutshell, technology enabled new services (or financial instruments) to be either proposed by institutions or demanded from the market.

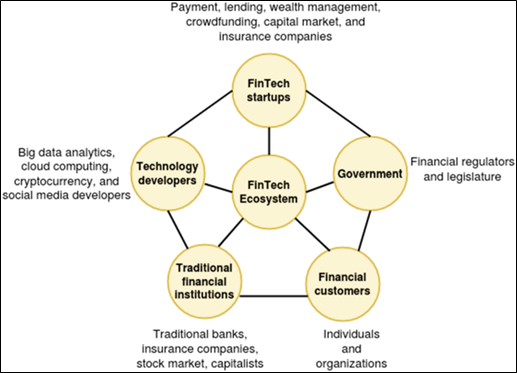

As an ecosystem, it extends over just the companies (usually startups), including the government, financial customers, traditional financial institutions, and technology developers, as Figure 1 shows. Briefly:

- Fintech startups are the companies that deliver innovation in the ecosystem.

- The Government embodies all the economic policies and development plans to stimulate innovation across the industry and ensure competition in the market. For example, it manages licensing of services, taxation, and capital requirements.

- The financial customers are all the individuals or organizations who typically use fintech products and services: they apply for mortgages or loans, adopt mobile payment apps, they engage through online platforms, and many more.

- The traditional financial institutions are the banks, stock markets and insurance companies, who integrate technology in their work environment.

- Technology developers are the providers of innovation, such as digital platforms, data analytics, cloud computing and many others.

Shifting the focus on the proper classification of Fintech companies, Caciatori et al. (2021) broke down the products and services offered by banks and Fintech startups in Brazil to identify nine categories of FinTechs:

- B2B

- Lending

- Digital Banks

- Payments and transfers

- Exchange

- Investments

- Insurance

- Advice

- Others (for example, loyalty programs or FX wholesale)

Among these, the most common would be the ‘Lending’, which includes a wide range of services like brokerage, capital debt and equity, credit, and mortgages. Alternatively, focusing on other contexts such as India and China, Vijai (2019) and Ye et al. (2022) identified four primary subfields to the field of financial technology:

- Financing (either credit, factoring or crowdfunding)

- Asset management (which includes also innovative fields like social trading and robo-advice)

- Payments (including blockchain, P2P payments and online banking)

- Other (for example, insurance, QR codes, or digital currencies for central banks)

The discrepancy in categorisation is likely to be caused by the already mentioned absence of an agreement over what FinTech is. Also, as the financial services industry became more and more integrated with each other, it is common for Fintechs to embody different categories, given the similarities in the underlying structure. For example, one of the first and most successful Fintech, PayPal, does not limit its offer just to online payments, but includes also money transfer, currency conversions, ‘Buy Now, Pay Later’ (essentially, consumer credit) and various other services to merchants, like payment buttons or integration with e-commerce platforms. This means it is possible and fair to classify PayPal in the category of B2B, lending, digital banks, exchange (according to the first set of categories), or both financing and payments, all considering PayPal is quite a ‘simple’ company, especially when compared to other players like the Chinese Alipay (which offers payment processing alongside wealth management, lending services, insurance products, and even social features).

So, I hope that the idea of Fintech being a subject worth exploring, whether you’re a recent graduate like me, a seasoned investor looking for the next big thing, or simply curious about how technology is revolutionizing finance, passed and is clear. In the upcoming articles of this series, we will dive into specific case studies, so stay tuned!

SOURCES

• Team, W.E. (2021). All About Fintech: History, Development, and Future. [online] Windmill. Available at: https://www.windmill.digital/all-about-fintech-history-development-and-future/ .

• Kaur, G., Habibi Lashkari, Z. and Habibi Lashkari, A. (2021). Introduction to FinTech and Importance Objects. Understanding Cybersecurity Management in FinTech, pp.1–15. doi: https://doi.org/10.1007/978-3-030-79915-1_1.

• Jabłoński, A. and Jabłoński, M. (2020) ‘Digital transformation and digital business models in the new economy. Network intelligence in the business models approach’, Studies in Economics and Finance, 37(4), pp. 753-770. Available at: https://www.emerald.com/insight/content/doi/10.1108/SEF-07-2019-0270/full/html (Accessed: 10 June 2024).

• Arner, D.W., Barberis, J.N. and Buckley, R.P. (2016) ‘The Evolution of Fintech: A New Post-Crisis Paradigm’, ResearchGate. Available at: https://www.researchgate.net/publication/313365410_The_Evolution_of_Fintech_A_New_Post-Crisis_Paradigm

• Caciatori Jr., I. and Mussi Szabo Cherobim, A.P. (2021). Defining categories of Fintechs: A Categorization Proposal Based on Literature and Empirical Data. Future Studies Research Journal: Trends and Strategies, 13(3), pp.386–408. doi: https://doi.org/10.24023/futurejournal/2175-5825/2021.v13i3.537.

• Vijai, C. (2019). Fintech in India – Opportunities and Challenges. SSRN Electronic Journal. doi: https://doi.org/10.2139/ssrn.3354094.

• Ye, Y., Chen, S. and Li, C. (2022). Financial technology as a driver of poverty alleviation in China: Evidence from an innovative regression approach. Journal of Innovation & Knowledge, 7(1), p.100164. doi: https://doi.org/10.1016/j.jik.2022.100164.

Image courtesy of Pexels / Pavel Danilyuk

Leave a comment